January 8, 2007

6:30 pm, (sharp)

393 Vintage Park Dr.

Suite 220

Foster City, CA. 94404

Map: http://tinyurl.com/yesb95

We are starting a PennyJar Investment Club in San Mateo and we would be thrilled to have you join us to find out more about what PennyJar is all about! Our first meeting is January 8, 2007. The location has lots of free parking and is easy to get to; just off highway 92.

Wednesday, December 27, 2006

Why US $ is going down: Central Banks buying Euros

The US dollar is having a hard time lately as its value continues to decline. One of the reasons is that foreign central banks are starting to diversify their holdings away from the US $ and toward the Euro. Remember the US government finances the deficit buy selling debt (US BONDS) and that the majority of the US Bonds are bought by foreign governments. This is because the US is viewed as a safe investment. However oil producing countries that are not exactly happy with the US are pushing hard to make the Euro the standard and not the US $.

Below is excerpt from news today

Reports that the United Arab Emirates would diversify its foreign currency reserves by purchasing more euros provided the currency-moving catalyst. Traders viewed the move as symptomatic of a wider trend and quickly bid up the euro.

"By itself, the UAE's shift is small change in the foreign-exchange market," Tony Crescenzi, chief bond market strategist at Miller Tabak and a RealMoney.com contributor, wrote in a published article. But "the UAE's shift is another in a string of actions taken by the world's central banks" to diversify away from the dollar.

source: the street.com http://www.thestreet.com/_iwon/markets/metals/10329783.html?cf=WSIWON1111051500

Below is excerpt from news today

Reports that the United Arab Emirates would diversify its foreign currency reserves by purchasing more euros provided the currency-moving catalyst. Traders viewed the move as symptomatic of a wider trend and quickly bid up the euro.

"By itself, the UAE's shift is small change in the foreign-exchange market," Tony Crescenzi, chief bond market strategist at Miller Tabak and a RealMoney.com contributor, wrote in a published article. But "the UAE's shift is another in a string of actions taken by the world's central banks" to diversify away from the dollar.

source: the street.com http://www.thestreet.com/_iwon/markets/metals/10329783.html?cf=WSIWON1111051500

Saturday, December 09, 2006

Friday, December 08, 2006

Someone tried to Scam me on Craigslist

I put an electric dryer for sale on Craigslist. Some guy offered me $140, which I accepted. He wanted to pay by certified check, which I also accepted (not too smart of me). I was thinking that a certified check is like cash.

Then I got this email, which smelled very bad to me:

Then I got this email, which smelled very bad to me:

Hi Paul,

How are you doing.Hope everything is going fine on your side, As a matter fact the deal is on and according to my secretary,he has already sent the check out to you.So the payment should arrive in a short while from now.And once you get it,i guess you know how to handle everything.And please dont bother about any other buyers.But there was a little problem which i guess we can handle with understanding.When i contacted my secretary to know maybe the payment as already been sent,i got to know that there was a misinterpretation while sending the payment.According to the instruction i gave him,he was suppose to have send you a check of $140.But instead,he sent a check of $1400. It was a terrible mistake and the check is already out for delivery to your location.But that should not disturb our own transaction.the deal is on and we will get through it.what will happen is that ,once you get the check you will take it to the bank and cash it immediately,then you deduct your $140, and a $25 dollars for your run around in cashing the check and also a $100 for sending the rest funds to my mover via western union money transfer that same day,my mover will be using the remaining funds for the pick up,i guess i can be assured in you that you can handle it with trust and have it sent to my mover.E-mail me back immediately to let me know that i can trust you to handle everything well.I will be expecting your e-mail asap.PLS AM PUTTING MY TRUST IN YOU.

Best Regards

and Stay Blessed.

Ken.I went to internet crime complaint center and found a description on COUNTERFEIT CASHIER'S CHECK. Basically, they get victims to wire money overseas via Western Union, after they think the check has cleared, but it really hasn't.

Then I called Wells Fargo to get advice on how to proceed, or not. They told me that the scammers work outside the country and they are getting away with it. They referred me to the Internet Crime Complaint Center. Unfortunately, the ICCC only keeps track of victims and are not proactive. They don't actually investigate, only keep statistics. Great.

I cancelled the deal. From now on I deal in cash only.

I can't help but think that a lot of people are falling for this crap.

Friday, December 01, 2006

How the Dollar System works

Lately I have been trying to learn more about why the US dollar is declining and see if I can figure out a safe haven for my investments if the dollar continues to decline. While searching the web I came across this well written and SCARY article about how the dollar system works and how it might be at the end of its life. This is a very thought provoking article and it made me think beyond my current understanding of the US economy. I encourage you to read and provide comments.

Thursday, November 30, 2006

Dizzy Dollar Data

One thing economists and financial reporters love to do is quote numbers.

In recent days, the "collapse" of the US dollar has been getting some headlines. A benchmark of the dollar is called the Dollar Index. It is an index created by the New York Board of Trade. It takes a basket of currencies and compares them to the US dollar. These currencies are "weighted", i.e. some have more effect than others on the index.

The currencies, and their respective weightings are:

Euro 57.6%

Yen 13.6%

Pound 11.9%

CAN dollar 9.1%

Swiss Franc 3.6%

Swedish Krona 4.2%

In theory, the NYBOT dollar index is trade weighted. That is to say the percentage of importance on the dollar index is a reflection of trade with America.

Well, I decided to look up the actual trade figures for last year, 2005.

Here's what I found.

In recent days, the "collapse" of the US dollar has been getting some headlines. A benchmark of the dollar is called the Dollar Index. It is an index created by the New York Board of Trade. It takes a basket of currencies and compares them to the US dollar. These currencies are "weighted", i.e. some have more effect than others on the index.

The currencies, and their respective weightings are:

Euro 57.6%

Yen 13.6%

Pound 11.9%

CAN dollar 9.1%

Swiss Franc 3.6%

Swedish Krona 4.2%

In theory, the NYBOT dollar index is trade weighted. That is to say the percentage of importance on the dollar index is a reflection of trade with America.

Well, I decided to look up the actual trade figures for last year, 2005.

Here's what I found.

- America's biggest trading partner was Canada. Almost $471 billion.

- America's second biggest trading partner was China. About $281 billion.

- All of Euro based Europe was somewhere over $300 billion.

Since the Euro makes up 57.6% of the index, one would think that we are doing a lot of trade with Europe. In fact, only about 11 or 12% of US trading activity is with (Euro) Europe. Canada, despite being weighted at 9.1% actually partners in 17% of US trade.

China isn't on the index. Neither is Mexico, which did over $270 billion in trade with the US. Korea and Taiwan combined did over $124 billion in trade. Also, you guessed it, NOT on the index.

Sweden and Switzerland, who make up 7.8% of the index did less than $39 billion last year, combined. That is a meagre 1.4% of US trade.

Perhaps the headline dollar index should be weighted to actual trade, not tied to some ratios that the NYBOT decides is reflective of the strength of the currency.

Bottom line is that headline numbers are often misleading. The dollar has fallen against the Euro and the Pound, but is that so bad, considering most of our foreign trade is done elsewhere? Maybe it hurts Europe more than America, particularly for tourism, airplanes and BMW's. Just a contrarian's view.

Simpler Times

At one time, the average American worker would get a job and earn money. He or she would save money in the bank to put a down payment on a house. The money in the bank would collect interest. They would buy a house and plan to have it all paid for in 20 to 30 years. The house would appreciate slightly better than inflation. Many of the companies they worked for provided pension plans. Workers did not have to be concerned with how these plans were invested; they only knew what to expect to be paid after their retirement.

Really sophisticated “investors” might have used some savings to buy securities, such as bonds or stocks. This was done with the help of a broker/advisor. There were a small number of mutual funds available to invest in. Some people bought investment properties with the intention of collecting rent (as opposed to flipping).

These days, there are so many, many choices for the individual, that it has become almost impossible for the average person to make any sense of it all. Many simply give up and surrender their money to multi-billion dollar management firms, which proceed to make outrageous amounts of profit from the management of your money, while your returns wallow in mediocrity.

Starting in January 2007, Pennyjar will be gathering small groups of individuals together to learn and gain confidence in personal finance and investing. These groups are in the form of an "investment club" but they will be much, much more than that. Our first groups will be in the San Francisco Bay area (since that's where we live).

It is important, to us, for people to be fully engaged in the process. For that reason, we will all have some "skin in the game". As a group we will be investing a small amount of money in real investments, be they stocks, bonds or some other product. Let's say, for the sake of argument, that each individual's minimum dollar comitment will be the equivavlent of about one Starbucks latte per week. Not too much, but it will be enough to make it interesting. The collective group of 10 or so members will decide on where the money gets specifically invested.

Pennyjar doesn't stop at being an investment club. We intend to make this process a lot of fun. By design, our meetings will be entertaining. There will also be a significant degree of social interaction. We are not interested in being a group of experts. Frankly, most of the supposed money "experts" are basically full of shit; they just know a lot of jargon and they know how to confuse people just enough so that they will be intimidated to hand over all thier money.

We are just regular people that want to get ahead and we agree that education and knowledge is the best path there. Better than lottery tickets, Amway, Vegas, dot.com stocks, pre-construction flips, and so on.

We are going to help people to help each other gain the knowledge and, we believe more importantly, the confidence to make good decisions. Pennyjar doesn't have all the answers, but we certainly will generate a lot of questions. And we will have a good time in the process.

We promise.

Really sophisticated “investors” might have used some savings to buy securities, such as bonds or stocks. This was done with the help of a broker/advisor. There were a small number of mutual funds available to invest in. Some people bought investment properties with the intention of collecting rent (as opposed to flipping).

These days, there are so many, many choices for the individual, that it has become almost impossible for the average person to make any sense of it all. Many simply give up and surrender their money to multi-billion dollar management firms, which proceed to make outrageous amounts of profit from the management of your money, while your returns wallow in mediocrity.

Starting in January 2007, Pennyjar will be gathering small groups of individuals together to learn and gain confidence in personal finance and investing. These groups are in the form of an "investment club" but they will be much, much more than that. Our first groups will be in the San Francisco Bay area (since that's where we live).

It is important, to us, for people to be fully engaged in the process. For that reason, we will all have some "skin in the game". As a group we will be investing a small amount of money in real investments, be they stocks, bonds or some other product. Let's say, for the sake of argument, that each individual's minimum dollar comitment will be the equivavlent of about one Starbucks latte per week. Not too much, but it will be enough to make it interesting. The collective group of 10 or so members will decide on where the money gets specifically invested.

Pennyjar doesn't stop at being an investment club. We intend to make this process a lot of fun. By design, our meetings will be entertaining. There will also be a significant degree of social interaction. We are not interested in being a group of experts. Frankly, most of the supposed money "experts" are basically full of shit; they just know a lot of jargon and they know how to confuse people just enough so that they will be intimidated to hand over all thier money.

We are just regular people that want to get ahead and we agree that education and knowledge is the best path there. Better than lottery tickets, Amway, Vegas, dot.com stocks, pre-construction flips, and so on.

We are going to help people to help each other gain the knowledge and, we believe more importantly, the confidence to make good decisions. Pennyjar doesn't have all the answers, but we certainly will generate a lot of questions. And we will have a good time in the process.

We promise.

Sunday, November 19, 2006

How to pick a stock: The BUD example

In a previous posting I covered how small-fish can buy stocks even if they do not have the $$ to open a brokerage account. The costs are not trivial; Etrade($1,000) and Charles Schwab($2,000). The answer was company direct stock purchase programs. For as little as $25 a month you can buy shares of ANHEUSER BUSCH (NYSE:BUD). How do you know if buying shares of BUD is a wise investment? The short answer is... you don't. No stock picker is right 100% of the time. However you can greatly increase your success rate by applying some basic stock analysis principles and understanding your risk tolerance. Risk tolerance is a way of measuring how you FEEL about risking your money for some reward. Usually a financial planner will asked you questions to help determine you risk tolerance. (or they should). Risk tolerance determines your investment style, conservative, moderate or aggressive. The higher your tolerance the more you are willing to accept some volatility in your investments. At the PennyJar we believe you should never invest any money you cannot afford to lose. Remember our talk about discretionary income?

Let's now turn our attention to analysing aka(understanding) ANHEUSER BUSCH (NYSE:BUD). Let's pretend we know nothing about buying stocks. What would be some of the things we would need to know? Well first what is a stock? When you buy a stock you are buying a piece of a company. Stock gives you partial ownership in a company. You become partners with the company. Your fortunes are tied to the company's success. It only seems logical then that you need to understand the company. Fundamental stock analysis is about understanding the company before you become a part owner in the company. O.K. what would I like to know about the company?

What does it do?

How does it make its money?

Can I go to sleep and know the company will still be there when I wake up?

Is the company profitable? (does it make more than it spends)

Does the company reward the stock holders by paying a dividend?

Who runs the company?

How effectively do the owners spend the stock holders money? Remember companies sell stock to raise money. What they do with this raised money is important to their business and your pockets.

Do we think the stock price will go up or down?

Getting the answers to these questions will help you decide if you should buy BUD.

The best place to look for the answer to our questions is Yahoo Finance. Here is the link to BUD at Yahoo Finance

What does it do? This can be found by clicking on profile link from Yahoo Finance. And here is where we find out that BUD "engages in the production and distribution of beer worldwide". This was not surprise (hopefully). We also find out "The Entertainment segment owns and operates theme parks. The company also is involved in the real estate development business; and owns and operates The Kingsmill Resort and Conference Center in Williamsburg, Virginia".

More I want more.. Let's visit www.hoovers.com to find out more about BUD. From Hoovers we find out that BUD owns a 50% stake in Mexico's top brewer, Grupo Modelo, which makes Corona and Negra Modelo among many other brands.

Let's stop here for now. Please look around the profile link. Can you tell me the name of the CEO and the income of th CEO? How many employees?

To be continued.........

Let's now turn our attention to analysing aka(understanding) ANHEUSER BUSCH (NYSE:BUD). Let's pretend we know nothing about buying stocks. What would be some of the things we would need to know? Well first what is a stock? When you buy a stock you are buying a piece of a company. Stock gives you partial ownership in a company. You become partners with the company. Your fortunes are tied to the company's success. It only seems logical then that you need to understand the company. Fundamental stock analysis is about understanding the company before you become a part owner in the company. O.K. what would I like to know about the company?

What does it do?

How does it make its money?

Can I go to sleep and know the company will still be there when I wake up?

Is the company profitable? (does it make more than it spends)

Does the company reward the stock holders by paying a dividend?

Who runs the company?

How effectively do the owners spend the stock holders money? Remember companies sell stock to raise money. What they do with this raised money is important to their business and your pockets.

Do we think the stock price will go up or down?

Getting the answers to these questions will help you decide if you should buy BUD.

The best place to look for the answer to our questions is Yahoo Finance. Here is the link to BUD at Yahoo Finance

What does it do? This can be found by clicking on profile link from Yahoo Finance. And here is where we find out that BUD "engages in the production and distribution of beer worldwide". This was not surprise (hopefully). We also find out "The Entertainment segment owns and operates theme parks. The company also is involved in the real estate development business; and owns and operates The Kingsmill Resort and Conference Center in Williamsburg, Virginia".

More I want more.. Let's visit www.hoovers.com to find out more about BUD. From Hoovers we find out that BUD owns a 50% stake in Mexico's top brewer, Grupo Modelo, which makes Corona and Negra Modelo among many other brands.

Let's stop here for now. Please look around the profile link. Can you tell me the name of the CEO and the income of th CEO? How many employees?

To be continued.........

Pardon me I just had a taxable event

- Losers that I have held for less than a year

- Winners that I have held for more than a year.

Why?

If you've held a stock for at least one year, you're eligible for long-term capital-gains rates. Long-term capital gains are taxed at the 20% rate for most folks, while short-term gains--or gains made on stocks held for less than one year--are taxed at ordinary income tax rates, which range from 15% to 39.6%. In my case I am in the 33% tax bracket. So by selling the winners I have held for a year or more I am saving about 13% in taxes compared to selling winners I have held for less than a year. "begin sidebar" see the potential tax draw backs of day-trading? "end sidebar" I decided to sell the losers I have held for less than a year so that I can claim the losses on this years taxes to help offset some of the gains. If my offer is accepted on the home, I will not enjoy the mortgage interest deduction until I do my 2006 taxes.

Wednesday, November 15, 2006

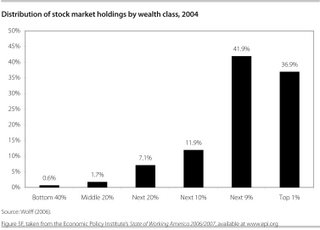

Who owns stock

Here at Pennyjar, when we talk about "little fish", we are referring to the middle class in this country. The fact of the matter is that right now in America the rich are getting richer and the middle class is treading water. This is statistical fact.

That said, does it really make sense to point at rich folks and blame them for your own current condition? Rather than blame, my strategy is to ask, "What are they doing?" and then do some of it. Blaming, or being a victim is disempowering. I find it more energizing to take some personal responsibility and change the habits that do not serve me well.

As you can see in the chart below, the top 10% weathiest people in America own roughly 80% of the stocks.

Maybe, if I want to be rich, I should know a little more about investing and stocks.

Maybe I should stop wasting my money on the latest gizmos, fashion trends or bling and put some of that money to work for me.

You think?

That said, does it really make sense to point at rich folks and blame them for your own current condition? Rather than blame, my strategy is to ask, "What are they doing?" and then do some of it. Blaming, or being a victim is disempowering. I find it more energizing to take some personal responsibility and change the habits that do not serve me well.

As you can see in the chart below, the top 10% weathiest people in America own roughly 80% of the stocks.

Maybe, if I want to be rich, I should know a little more about investing and stocks.

Maybe I should stop wasting my money on the latest gizmos, fashion trends or bling and put some of that money to work for me.

You think?

Sunday, November 12, 2006

NASD tools: Check your Broker & Mutual Fund fees

Here is the quick tip of the day. You can check the license or disciplinary history of your broker or securities firm online by going to the "NASDS BrokerCheck" section of the NASD's website. Here is the link to online broker check. This site is also packed with information such as latest investment scams and a GREAT tool for comparing mutual funds for their cost. This is a MUST see if you own or are thinking of buying some mutual funds. The fees associated with mutual funds eat away at your real returns.

Tuesday, November 07, 2006

Mortgage con artists

This piece from CNN/Money on mortgage fraud is a MUST READ!

A lot of ordinary, well meaning folks are being taken to the cleaners by sweet talking con men. The government is trying to crack down, but their results are not very good so far.

Your best defense is knowledge.

Understand the con and render the artist impotent.

A lot of ordinary, well meaning folks are being taken to the cleaners by sweet talking con men. The government is trying to crack down, but their results are not very good so far.

Your best defense is knowledge.

Understand the con and render the artist impotent.

"Since the housing market started to soar in 2001, mortgage fraud has become the fastest-growing white-collar crime, according to the FBI. Last year crooks skimmed at least $1 billion from the $3 trillion U.S. mortgage market.This slideshow gives a summary of some of the common cons, including the "Rent to Steal", "Straw man swindle" and the "Million dollar dump".Now that the market is slowing, fraud is only rising. As business dries up, there's increasing pressure on lenders, brokers, title companies and appraisers to be profitable. That means loan and title documents aren't scrutinized as carefully as they might be, and courts - many of them so low-tech they resemble Mayberry - can't keep up with the volume of paper.

Then there's the mad rush to sell, particularly by people who paid high prices for homes and suddenly can't afford the mortgages.

It's like a tasting menu for con artists and grifters, so tempting that in some cities drug dealers have turned to mortgage fraud, plaguing lower-income neighborhoods with crooked mortgages rather than crystal meth."

Friday, November 03, 2006

Put Your Money Where Your Mouth Is

How many fund managers invest in thier own funds?

According to WSJ article today:

"It has become easier to know this thanks to a rule by the Securities and Exchange Commission that required fund companies, starting last year, to disclose whether fund managers hold stakes in funds they run. This information can generally be found in a fund's "statement of additional information," posted on a fund company's Web site. The data are given in broad dollar ranges -- specifying only if a manager has invested, say, "$1 to $10,000" in a fund, or "over $1,000,000.""

I went fishing to see how easy it is to get this information. I spent almost an hour on two mutual fund websites and scanned through some prospectus looking for disclosure of managers' "skin in the game".

Alas, I failed, miserably. I will return later to the quest.

According to WSJ article today:

"It has become easier to know this thanks to a rule by the Securities and Exchange Commission that required fund companies, starting last year, to disclose whether fund managers hold stakes in funds they run. This information can generally be found in a fund's "statement of additional information," posted on a fund company's Web site. The data are given in broad dollar ranges -- specifying only if a manager has invested, say, "$1 to $10,000" in a fund, or "over $1,000,000.""

I went fishing to see how easy it is to get this information. I spent almost an hour on two mutual fund websites and scanned through some prospectus looking for disclosure of managers' "skin in the game".

Alas, I failed, miserably. I will return later to the quest.

Tuesday, October 31, 2006

Simplifying Paperwork

Big brokerage firms are starting to clue in that people are overwhelmed by the amount of paperwork and disclosures they have to deal with. Firms trying to make correspondence in "better English" are Bank of America, Morgan Stanley, Wachovia and Smith Barney (Citigroup). Excerpt from the WSJ below:

Wall Street Aims to Simplify

Disclosures for Clients

By JAIME LEVY PESSIN

October 31, 2006; Page D2

NEW YORK -- New Morgan Stanley customers will no longer have to read through 14 documents -- amounting to 136 pages -- to get their accounts running. Soon, their financial advisers will hand them a single, 48-page document.

Streamlining efforts like Morgan Stanley's are under way at several Wall Street firms, an acknowledgment that firms -- while satisfying a legal obligation to disclose information -- aren't necessarily informing or educating their customers.

The brokerage industry has an obligation to make multiple disclosures to their clients. Product prospectuses, possible conflicts of interest and the distinctions between fee-based brokerage and advisory accounts, among other things, must be disclosed at various stages of brokerage and advisory relationships.

Bill Lutz, a professor emeritus at Rutgers University who consults regulators and financial firms on incorporating plain language into disclosures, said he has seen companies lose clients because investors were exasperated by the lack of clarity.

Not only do more-understandable disclosures make for better customer service, he said, they reduce firms' liability in cases where customers claim they don't understand what they have signed.

"People have successfully argued, 'We just didn't understand what you were telling us,' " Mr. Lutz said.

Wall Street Aims to Simplify

Disclosures for Clients

By JAIME LEVY PESSIN

October 31, 2006; Page D2

NEW YORK -- New Morgan Stanley customers will no longer have to read through 14 documents -- amounting to 136 pages -- to get their accounts running. Soon, their financial advisers will hand them a single, 48-page document.

Streamlining efforts like Morgan Stanley's are under way at several Wall Street firms, an acknowledgment that firms -- while satisfying a legal obligation to disclose information -- aren't necessarily informing or educating their customers.

The brokerage industry has an obligation to make multiple disclosures to their clients. Product prospectuses, possible conflicts of interest and the distinctions between fee-based brokerage and advisory accounts, among other things, must be disclosed at various stages of brokerage and advisory relationships.

Bill Lutz, a professor emeritus at Rutgers University who consults regulators and financial firms on incorporating plain language into disclosures, said he has seen companies lose clients because investors were exasperated by the lack of clarity.

Not only do more-understandable disclosures make for better customer service, he said, they reduce firms' liability in cases where customers claim they don't understand what they have signed.

"People have successfully argued, 'We just didn't understand what you were telling us,' " Mr. Lutz said.

Saturday, October 28, 2006

Hacking of online brokerage accounts starts to grow

According to a report in Moneywatch.com there has been a recent increase in the hacking of online brokerage accounts. The article points out the risk of using public computers to access your accounts. We are talking about any computer that you do not have control over. This includes a computer at a hotel, library or Internet Cafe. Hackers can load keystoke logging software onto these computers and capture your username and password.

Foul Fish Report

I subscribe to a couple of financial news mailing list. Everyday my inbox gets filled with the day’s happenings in the world of finance. Unfortunately I am too busy to read these stories everyday and I end up dragging the emails to a “save for later” folder. Today I thought it would be interesting to go through my “save for later” folder of financial news and dig out all the negative stories. I call this inaugural list of wrong doings, “The Foul Fish Report”, in keeping with the Pennyjar little fish vs. BIG fish theme.

I subscribe to a couple of financial news mailing list. Everyday my inbox gets filled with the day’s happenings in the world of finance. Unfortunately I am too busy to read these stories everyday and I end up dragging the emails to a “save for later” folder. Today I thought it would be interesting to go through my “save for later” folder of financial news and dig out all the negative stories. I call this inaugural list of wrong doings, “The Foul Fish Report”, in keeping with the Pennyjar little fish vs. BIG fish theme.Sept. 13 HP CEO Patricia Dunn resigns.

Her efforts to catch boardroom leakers last year led the Palo Alto, Calif., company to hire a contractor that scrutinized the private phone records of H-P's own directors and nine journalists.

Sept. 22 Dead guy gets stock

Cablevision Systems Corp. awarded options to a vice chairman after his 1999 death but backdated them, making it appear the grant was awarded when he still was alive

Sept. 27 Health insurance premiums rise 7.7%

The WSJ reports The average family premium rose 7.7% in 2006. That compared with a 3.8% rise in wages and inflation of around 3.5%.

Oct. 4 Intel investigation.

WSJ reports European Union investigators believe they have enough evidence to pursue formal antitrust charges against Intel Corp., a critical step in their five-year probe of the computer-chip maker, according to two people with knowledge of the case.

Oct. 4 Down on Dunn

HP Chairperson Patricia Dunn was named in felony complaints in California Wednesday along with four others related to a mole hunt undertaken at Hewlett-Packard while she was chairwoman of the computer maker

Oct. 4 401(k) fees too high

St. Louis attorney sued seven big employers-- Bechtel Group, Caterpillar, Exelon, General Dynamics, International Paper, Northrop Grumman and United Technologies--for allegedly allowing their employees' 401(k) plans to be hit with too-high fees, in violation of the Employee Retirement Income Security Act (ERISA).

Oct. 10 Tip of the Iceberg

The Department of Justice has begun an inquiry into potentially anticompetitive behavior among some of the world's leading private-equity funds (WSJ)

Oct. 15 Hey you caught me!

United Health CEO William McGuire plans to retire in the wake of a probe of the company's past stock-options grants. At the end of last year, Dr. McGuire's cache of unexercised options was valued at $1.78 billion. “Hey let me steal $1.78 billion and I would take the punishment of having to retire.” The beat goes on and on with this story. Here is latest list of 120 companies under scrutiny for past stock-option grants

Oct. 20 No bonuses for Costco execs

President and Chief Executive Jim Sinegal and Chief Financial Officer Richard Galanti won't receive bonuses this year.

Oct. 24 Guilty

David Kreinberg pleaded guilty to securities-fraud charges in federal court in New York. The former finance chief of Comverse Technology is the first person to plead guilty in the stock-options backdating scandal.

Oct. 24 Yikes! What happened to FORD?

Ford Motor Co.'s $5.8 billion third-quarter preliminary net loss

Oct. 26 Mutual-fund kickbacks

The SEC has launched a probe of 27 mutual-fund companies that the agency says have accepted kickbacks totaling hundreds of millions of dollars.

Oct. 26 Slick OIL.

Exxon's profit rose to $10.49 billion in the third quarter, the second-highest quarterly profit ever for a publicly traded U.S. company.

Friday, October 27, 2006

WSJ Piece on Latest Mutual Fund Investigation

SEC Probes Mutual-Fund Firms

After Settlement in Kickback Case

By TOM LAURICELLA

October 26, 2006; Page A1

The Securities and Exchange Commission has launched an investigation of 27 mutual-fund companies that the agency says have accepted kickbacks totaling hundreds of millions of dollars in recent years.

The investigation centers on alleged arrangements in which independent contractors agreed to pay rebates to mutual-fund companies in order to win lucrative contracts for jobs like producing shareholder reports and prospectuses. The probe stems from a $21.4 million settlement the SEC reached last month with Bisys Fund Services Inc., an administrative-services provider owned by Bisys Group Inc.

Regulators say Bisys, which is based in Roseland, N.J., paid a total of $230 million in kickbacks between July 1999 and June 2004 as part of an effort to win work from mutual funds. Bisys settled the civil charges without admitting or denying wrongdoing.

While the alleged kickbacks would have taken only a tiny toll on individual investors, perhaps shaving a few hundredths of a percent a year off their fund accounts and returns, the latest investigation comes as the fund industry is struggling to rebuild its reputation after a series of trading scandals that triggered regulatory crackdowns and fines totaling more than $1 billion.

Critics have long complained about fund companies using shareholder money for their own benefit. For example, funds are allowed to use trading commissions, which are deducted from shareholder funds, to pay for research that may not benefit individual fund investors. They can also levy fees on their investors for marketing, although attracting more investors benefits the fund company and not necessarily its existing shareholders. Both these practices are highly regulated to prevent abuses. Nonetheless, regulators and other observers say the latest scandal is part of a distressing pattern of fund companies misusing shareholder money.

"This is far worse conduct" than previous fund-trading scandals, said Mercer Bullard, a law professor at the University of Mississippi who specializes in mutual-fund matters. "Receiving a kickback that comes indirectly out of the pockets of shareholders is the functional equivalent of embezzlement."

In part based on information from Bisys, the SEC has sent letters to some of the 27 fund companies asking them to provide details about their ties to Bisys, according to people familiar with the probe. They didn't identify any of the companies. However, the investigation is unlikely to include many of the very largest fund companies, which tend to have in-house units that handle administrative functions.

Most of Bisys's clients were bank-run funds, many of which tended to be smaller firms with several billion of dollars under management. A handful of banks, however, do rank among the larger fund managers.

The SEC says the alleged kickbacks involving Bisys and other service providers worked with the help of secret side agreements. The service providers charged shareholder accounts for administrative services but, unbeknownst to the funds' investors or independent board members, the providers agreed to rebate part of that money to fund advisers, who would then use it to cover their marketing expenses. In exchange for the kickbacks, the advisers would recommend to their funds' boards that the service providers' contracts be renewed.

At issue in the probe is whether fund companies misused their investors' money and misled their boards about why they were hiring certain service providers, according to people familiar with the probe. "These matters raise questions about whether there was a breach of duty to shareholders," said Philip Khinda, an attorney who represents a number of fund boards that have been investigating their funds' arrangements with Bisys.

In its complaint against Bisys, the SEC described the actions of one fund company, which it referred to as "Adviser A," that allegedly demanded millions of dollars in kickbacks in return for recommending that Bisys's contract be renewed. Another 26 fund families had similar deals -- some written, and some only oral -- with the firm, the SEC said.

The agency didn't identify any of the fund companies in the complaint but, according to people familiar with the investigation, "Adviser A" is AmSouth Funds, which was then a unit of AmSouth Bancorp of Birmingham, Ala.

AmSouth Bancorp declined to comment on whether or not it is the company referred to as "Adviser A," but it said it is cooperating with the SEC.

In 2005, after the alleged arrangement with Bisys had ended, the AmSouth Funds, which then totaled $5.5 billion in assets, were sold to Pioneer Investments. A spokesman for Pioneer declined to comment.

The SEC's Bisys complaint says a senior executive at "Adviser A" told Bisys in 1999 that if it didn't agree to a kickback arrangement, one of its competitors would. Indeed, the SEC alleged in its complaint that "other administrators" besides Bisys cut such deals.

Bisys's main competitor is SEI Investments Co. A spokesman for SEI, which is based in Oaks, Pa., said that as a matter of policy the company wouldn't comment on whether it had received inquiries from the SEC nor on whether it had similar rebate agreements with fund companies.

Bisys accepted the deal with "Adviser A," and over the next five years, funds totaling $17.3 million were deducted from shareholder accounts at the fund company, according to the SEC. The money was used by "Adviser A" mainly to cover marketing costs that would normally come out of its own pocket. The adviser also used some of the money to pay the initiation fee and monthly dues at a country club, the SEC's complaint says.

In the arrangement with "Adviser A," Bisys would be paid 0.20% of fund's assets, the SEC said. However, Bisys kept only roughly one-quarter of that amount. About one-third was paid to "Adviser A" in an above-board contract, the SEC says, while the remainder was kicked back to the adviser through a "marketing budget."

In its settlement with the SEC, Bisys agreed to terminate such agreements and change its policies. It disciplined or fired a number of employees.

Last summer, AmSouth gave its own version of its dealings with Bisys. At the time, it disclosed that the SEC had informed the bank it intended to bring civil charges against it related to the service provider. It said that the probe related to "past arrangements under which Bisys used a portion of the fees paid to it by the fund family to pay for marketing and other expenses."

The mutual-fund industry has been dogged by scandals in recent years. In 2003, it came under fire after revelations that a number of big companies let favored clients conduct short-term trading, earning profits at the expense of ordinary shareholders. The following year, regulators cracked down on fund companies that used stock-trading commissions, which are deducted from shareholder accounts, to pay for marketing activities the companies would otherwise have had to cover themselves.

After Settlement in Kickback Case

By TOM LAURICELLA

October 26, 2006; Page A1

The Securities and Exchange Commission has launched an investigation of 27 mutual-fund companies that the agency says have accepted kickbacks totaling hundreds of millions of dollars in recent years.

The investigation centers on alleged arrangements in which independent contractors agreed to pay rebates to mutual-fund companies in order to win lucrative contracts for jobs like producing shareholder reports and prospectuses. The probe stems from a $21.4 million settlement the SEC reached last month with Bisys Fund Services Inc., an administrative-services provider owned by Bisys Group Inc.

Regulators say Bisys, which is based in Roseland, N.J., paid a total of $230 million in kickbacks between July 1999 and June 2004 as part of an effort to win work from mutual funds. Bisys settled the civil charges without admitting or denying wrongdoing.

While the alleged kickbacks would have taken only a tiny toll on individual investors, perhaps shaving a few hundredths of a percent a year off their fund accounts and returns, the latest investigation comes as the fund industry is struggling to rebuild its reputation after a series of trading scandals that triggered regulatory crackdowns and fines totaling more than $1 billion.

Critics have long complained about fund companies using shareholder money for their own benefit. For example, funds are allowed to use trading commissions, which are deducted from shareholder funds, to pay for research that may not benefit individual fund investors. They can also levy fees on their investors for marketing, although attracting more investors benefits the fund company and not necessarily its existing shareholders. Both these practices are highly regulated to prevent abuses. Nonetheless, regulators and other observers say the latest scandal is part of a distressing pattern of fund companies misusing shareholder money.

"This is far worse conduct" than previous fund-trading scandals, said Mercer Bullard, a law professor at the University of Mississippi who specializes in mutual-fund matters. "Receiving a kickback that comes indirectly out of the pockets of shareholders is the functional equivalent of embezzlement."

In part based on information from Bisys, the SEC has sent letters to some of the 27 fund companies asking them to provide details about their ties to Bisys, according to people familiar with the probe. They didn't identify any of the companies. However, the investigation is unlikely to include many of the very largest fund companies, which tend to have in-house units that handle administrative functions.

Most of Bisys's clients were bank-run funds, many of which tended to be smaller firms with several billion of dollars under management. A handful of banks, however, do rank among the larger fund managers.

The SEC says the alleged kickbacks involving Bisys and other service providers worked with the help of secret side agreements. The service providers charged shareholder accounts for administrative services but, unbeknownst to the funds' investors or independent board members, the providers agreed to rebate part of that money to fund advisers, who would then use it to cover their marketing expenses. In exchange for the kickbacks, the advisers would recommend to their funds' boards that the service providers' contracts be renewed.

At issue in the probe is whether fund companies misused their investors' money and misled their boards about why they were hiring certain service providers, according to people familiar with the probe. "These matters raise questions about whether there was a breach of duty to shareholders," said Philip Khinda, an attorney who represents a number of fund boards that have been investigating their funds' arrangements with Bisys.

In its complaint against Bisys, the SEC described the actions of one fund company, which it referred to as "Adviser A," that allegedly demanded millions of dollars in kickbacks in return for recommending that Bisys's contract be renewed. Another 26 fund families had similar deals -- some written, and some only oral -- with the firm, the SEC said.

The agency didn't identify any of the fund companies in the complaint but, according to people familiar with the investigation, "Adviser A" is AmSouth Funds, which was then a unit of AmSouth Bancorp of Birmingham, Ala.

AmSouth Bancorp declined to comment on whether or not it is the company referred to as "Adviser A," but it said it is cooperating with the SEC.

In 2005, after the alleged arrangement with Bisys had ended, the AmSouth Funds, which then totaled $5.5 billion in assets, were sold to Pioneer Investments. A spokesman for Pioneer declined to comment.

The SEC's Bisys complaint says a senior executive at "Adviser A" told Bisys in 1999 that if it didn't agree to a kickback arrangement, one of its competitors would. Indeed, the SEC alleged in its complaint that "other administrators" besides Bisys cut such deals.

Bisys's main competitor is SEI Investments Co. A spokesman for SEI, which is based in Oaks, Pa., said that as a matter of policy the company wouldn't comment on whether it had received inquiries from the SEC nor on whether it had similar rebate agreements with fund companies.

Bisys accepted the deal with "Adviser A," and over the next five years, funds totaling $17.3 million were deducted from shareholder accounts at the fund company, according to the SEC. The money was used by "Adviser A" mainly to cover marketing costs that would normally come out of its own pocket. The adviser also used some of the money to pay the initiation fee and monthly dues at a country club, the SEC's complaint says.

In the arrangement with "Adviser A," Bisys would be paid 0.20% of fund's assets, the SEC said. However, Bisys kept only roughly one-quarter of that amount. About one-third was paid to "Adviser A" in an above-board contract, the SEC says, while the remainder was kicked back to the adviser through a "marketing budget."

In its settlement with the SEC, Bisys agreed to terminate such agreements and change its policies. It disciplined or fired a number of employees.

Last summer, AmSouth gave its own version of its dealings with Bisys. At the time, it disclosed that the SEC had informed the bank it intended to bring civil charges against it related to the service provider. It said that the probe related to "past arrangements under which Bisys used a portion of the fees paid to it by the fund family to pay for marketing and other expenses."

The mutual-fund industry has been dogged by scandals in recent years. In 2003, it came under fire after revelations that a number of big companies let favored clients conduct short-term trading, earning profits at the expense of ordinary shareholders. The following year, regulators cracked down on fund companies that used stock-trading commissions, which are deducted from shareholder accounts, to pay for marketing activities the companies would otherwise have had to cover themselves.

Wednesday, October 18, 2006

Brokers cost you Billions

I have been reading a study by Daniel Bergstresser and Peter Tufano, both at Harvard Business School, and the University of Oregon's John Chalmers.

The reports compares the performance of mutual funds bought through a broker compared to funds bought directly. The conclusion is that, through brokers, "consumers pay extra distribution fees to buy funds with non-distribution expenses. The funds they buy under perform those in the direct channel, even before deductions of any distribution related expenses."

Statistics don't lie. The statistics say that, by using a broker, you are

1. paying higher sales fees

2. to buy funds with higher management fees

3. that get crappy returns.

The crappy returns cost investors approximately $9 billion per year, and that is not including distribution expenses.

Why is this happening?

I go to the section 9, titled "Do Brokers Merely Sell what they are Paid to Sell?

Here, the authors refer to the obvious hypothesis that "brokers may give priority to their self-interest or to the interests of the management companies whose funds they sell."

The statistical evidence indicates that higher fees paid to brokers result in higher sales for the mutual fund paying the fee. According to the report, "These results suggest that sales incentives are more effective in the broker channel, consistent with the old saw that funds are sold, not bought - and that paying a salesforce on a higher piece-rate scale may induce additional sales"

Ultimately, all the fees and commissions come from the investors. Your money.

Do you know what you are paying in fees?

Do you know how much of your money your broker is getting?

The reports compares the performance of mutual funds bought through a broker compared to funds bought directly. The conclusion is that, through brokers, "consumers pay extra distribution fees to buy funds with non-distribution expenses. The funds they buy under perform those in the direct channel, even before deductions of any distribution related expenses."

Statistics don't lie. The statistics say that, by using a broker, you are

1. paying higher sales fees

2. to buy funds with higher management fees

3. that get crappy returns.

The crappy returns cost investors approximately $9 billion per year, and that is not including distribution expenses.

Why is this happening?

I go to the section 9, titled "Do Brokers Merely Sell what they are Paid to Sell?

Here, the authors refer to the obvious hypothesis that "brokers may give priority to their self-interest or to the interests of the management companies whose funds they sell."

The statistical evidence indicates that higher fees paid to brokers result in higher sales for the mutual fund paying the fee. According to the report, "These results suggest that sales incentives are more effective in the broker channel, consistent with the old saw that funds are sold, not bought - and that paying a salesforce on a higher piece-rate scale may induce additional sales"

Ultimately, all the fees and commissions come from the investors. Your money.

Do you know what you are paying in fees?

Do you know how much of your money your broker is getting?

Coming Up Short

Mutual-fund investors' real results are often surprisingly poor.

• Over the past 10 years, owners of diversified U.S. stock funds collected 7.3% a year, less than their funds' 8.8% published return.

• In 19 stock markets, investors underperformed a buy-and-hold strategy by 1.5 percentage points a year since 1973.

• Over seven years, broker-sold stock funds lagged behind directly sold funds by half a percentage point a year after expenses.

Sources: Morningstar Inc.; academic studies

• Over the past 10 years, owners of diversified U.S. stock funds collected 7.3% a year, less than their funds' 8.8% published return.

• In 19 stock markets, investors underperformed a buy-and-hold strategy by 1.5 percentage points a year since 1973.

• Over seven years, broker-sold stock funds lagged behind directly sold funds by half a percentage point a year after expenses.

Sources: Morningstar Inc.; academic studies

Tuesday, October 17, 2006

130/30

So what is the 130/30 strategy?

Let's start at the beginning. The "Alpha".

I am not referring to the first letter of the alphabet or the biggest gorilla in the troupe. In finance, alpha has a different meaning.

It is a measure of how well an investment, usually a mutual fund, performs in comparison to the overall market. In an oversimplified example, if the whole market goes up 10% and your specific investment goes up 10%, then the alpha of that investement would be zero.

Things get a little more complicated because Alpha also considers the relative risk of whatever stocks are being bought. If a fund manager invests in stocks that are very stable (i.e. prices don't fluctuate too much), the alpha is calculated differently than if the fund manager invests in very volatile stocks.

Conventional wisdom states:

Stable stocks are safer - volatile stocks are riskier.

Therefore, if one invests in risky stocks, the potential profits should be higher. Alpha takes that into consideration. A mutual fund specializing in nanotechnology start ups would have to deliver much higher profits than a collection of blue chip mega-corporations to get the same "alpha" ranking.

So, getting back to 130/30. The goal is to increase the alpha while maintaining low volatility. It works like this:

Let's assume $100 investment.

1. Buy $100 of large cap stocks

2. Sell short $30 of the stocks in your portfolio

3. Take the proceeds of the short sale and buy more large cap stocks.

Confusing? Just a bit. Selling short is like betting that a share price will go down. How this is achieved can be complex and possibly another post on the blog. These days, shorting often involves trading of options and derivatives. The important thing to know is that the more a stock falls, the more profit the investor makes.

The tacit assumption is that the managers of the 130/30 fund are good at picking winner and loser stocks. Ultimately, that is going to determine performance.

The cool thing is that this strategy limits losses when markets turn downward. This is how risk is reduced, without sacrificing performance. It could limit profits in a crazy bull market. But in the long race, it is often profitable to bet on the tortoise, not the hare.

Let's start at the beginning. The "Alpha".

I am not referring to the first letter of the alphabet or the biggest gorilla in the troupe. In finance, alpha has a different meaning.

It is a measure of how well an investment, usually a mutual fund, performs in comparison to the overall market. In an oversimplified example, if the whole market goes up 10% and your specific investment goes up 10%, then the alpha of that investement would be zero.

Things get a little more complicated because Alpha also considers the relative risk of whatever stocks are being bought. If a fund manager invests in stocks that are very stable (i.e. prices don't fluctuate too much), the alpha is calculated differently than if the fund manager invests in very volatile stocks.

Conventional wisdom states:

Stable stocks are safer - volatile stocks are riskier.

Therefore, if one invests in risky stocks, the potential profits should be higher. Alpha takes that into consideration. A mutual fund specializing in nanotechnology start ups would have to deliver much higher profits than a collection of blue chip mega-corporations to get the same "alpha" ranking.

So, getting back to 130/30. The goal is to increase the alpha while maintaining low volatility. It works like this:

Let's assume $100 investment.

1. Buy $100 of large cap stocks

2. Sell short $30 of the stocks in your portfolio

3. Take the proceeds of the short sale and buy more large cap stocks.

Confusing? Just a bit. Selling short is like betting that a share price will go down. How this is achieved can be complex and possibly another post on the blog. These days, shorting often involves trading of options and derivatives. The important thing to know is that the more a stock falls, the more profit the investor makes.

The tacit assumption is that the managers of the 130/30 fund are good at picking winner and loser stocks. Ultimately, that is going to determine performance.

The cool thing is that this strategy limits losses when markets turn downward. This is how risk is reduced, without sacrificing performance. It could limit profits in a crazy bull market. But in the long race, it is often profitable to bet on the tortoise, not the hare.

Monday, October 16, 2006

Hedging Stocks

Many millions of ordinary people have, over the past 25 years, been steadily bombarded with the voices of conventional wisdom telling them over and over how stocks outperform every other form of investment. They have collectively entrusted their individual retirement accounts to the markets.

Alternately, they have entrusted their public retirement benefits, namely social security and medicare, to the government. The government has mismanaged these programs and now finds itself with trillions of dollars of unfunded liabilities, going forward. (i.e. the system is headed for bankruptcy)

Hmm. Stock market and government. Who should we trust less?

I would contend that people can, really and truly, only depend upon THEMSELVES. To trust politicians and Wall Street sharks to take care of your money has got to be the height of mass gullibility. Ordinary people learning to take care of their own financial lives is why we started Pennyjar. It's not as complicated as the "experts" would have you believe; and it can be fun, with the right approach.

But I digress.

It is quite true that one can become very wealthy through owning stocks, but for the majority of us, it simply has not come true. So many ordinary people lost money in the dot.com bust. So many ordinary people have watched their mutual fund based retirement portfolios wallow in mediocrity since the bull market ended in 2000.

So who is really making money with stock?

In very basic terms, there is a class system in play in this country.

The working class has basically nothing. They are living paycheck to paycheck and are prisoners of debt. They are depending on social security and medicare to take care of them after they finish working. There are some uncertain times ahead for this group of 50 million or so unfortunate Americans. Fact of the matter is that they may not be able to retire and will probably have to keep working to make ends meet, until they cannot.

The middle class has invested trillions of dollars in mutual funds, most of them invested in a basket of US stocks. When stocks go up, they win. When stocks go down, they lose. Very simple game. Of course, the brokers, investment advisors, mutual funds, corporate executives and tax man all win, no matter what. All the risk of loss is in the hands of the individual holding the stocks (i.e.: YOU).

The rich are a very different story. The rich, that is to say, people with a liquid net worth of more than a $ million, are able to be designated as “Accredited Investors” and can invest their money in “private equity funds”, often better known as hedge funds. They, like the middle class, buy stocks with the anticipation that they will go up in value. Unlike the middle class, however, rich investors also may have a percentage of their investments configured so that if stock prices drop, they also make money. This is known as hedging and is where name “hedge funds” originated.

So what can you do if, like most ordinary people, you don’t have over a million dollars available for investing? To begin with, it is possible to do some hedging of your own.

There are some relatively new products available. Some in particular caught my eye recently. They are newer mutual funds utilizing a 130/30 strategy. It is a strategy that hedges against stocks going down and is available for ordinary people. The managers of these funds "short" 30% of theirs stocks. I will post more on 130/30 strategy later.

There are also some relatively new ETFs (exchange traded funds) that are engineered to move inversely with the market. That is to say, if the market drops, the ETF goes up. If the market goes up, the ETF goes down.

Using hedging as a strategy is most certainly not good for everyone. But it is an option, and it is utilized by a lot of very rich people, so there must be something in it.

Alternately, they have entrusted their public retirement benefits, namely social security and medicare, to the government. The government has mismanaged these programs and now finds itself with trillions of dollars of unfunded liabilities, going forward. (i.e. the system is headed for bankruptcy)

Hmm. Stock market and government. Who should we trust less?

I would contend that people can, really and truly, only depend upon THEMSELVES. To trust politicians and Wall Street sharks to take care of your money has got to be the height of mass gullibility. Ordinary people learning to take care of their own financial lives is why we started Pennyjar. It's not as complicated as the "experts" would have you believe; and it can be fun, with the right approach.

But I digress.

It is quite true that one can become very wealthy through owning stocks, but for the majority of us, it simply has not come true. So many ordinary people lost money in the dot.com bust. So many ordinary people have watched their mutual fund based retirement portfolios wallow in mediocrity since the bull market ended in 2000.

So who is really making money with stock?

In very basic terms, there is a class system in play in this country.

The working class has basically nothing. They are living paycheck to paycheck and are prisoners of debt. They are depending on social security and medicare to take care of them after they finish working. There are some uncertain times ahead for this group of 50 million or so unfortunate Americans. Fact of the matter is that they may not be able to retire and will probably have to keep working to make ends meet, until they cannot.

The middle class has invested trillions of dollars in mutual funds, most of them invested in a basket of US stocks. When stocks go up, they win. When stocks go down, they lose. Very simple game. Of course, the brokers, investment advisors, mutual funds, corporate executives and tax man all win, no matter what. All the risk of loss is in the hands of the individual holding the stocks (i.e.: YOU).

The rich are a very different story. The rich, that is to say, people with a liquid net worth of more than a $ million, are able to be designated as “Accredited Investors” and can invest their money in “private equity funds”, often better known as hedge funds. They, like the middle class, buy stocks with the anticipation that they will go up in value. Unlike the middle class, however, rich investors also may have a percentage of their investments configured so that if stock prices drop, they also make money. This is known as hedging and is where name “hedge funds” originated.

So what can you do if, like most ordinary people, you don’t have over a million dollars available for investing? To begin with, it is possible to do some hedging of your own.

There are some relatively new products available. Some in particular caught my eye recently. They are newer mutual funds utilizing a 130/30 strategy. It is a strategy that hedges against stocks going down and is available for ordinary people. The managers of these funds "short" 30% of theirs stocks. I will post more on 130/30 strategy later.

There are also some relatively new ETFs (exchange traded funds) that are engineered to move inversely with the market. That is to say, if the market drops, the ETF goes up. If the market goes up, the ETF goes down.

Using hedging as a strategy is most certainly not good for everyone. But it is an option, and it is utilized by a lot of very rich people, so there must be something in it.

Sunday, October 15, 2006

San Mateo County: Renters beware!

Developers are not building new rental units in San Mateo county and many landlords are converting their apartment buildings to for-sale units. Why? The high cost of building in San Mateo county. When developers build condos they can sell them and see an immediate return on their investment. Rental properties can take years to break-even. Full story can be found at condo construction outpacing rentals. The end result will be an acute shortage of rental units. This means that rents will go up. According to the housing Leadership Council of San Mateo County the median price for a 2-BR apartment is $1,536 while the median mortgage on a condo is $3,239 ($550,00 & 30yr mortgage). I have been counting on the spread between owning[$3,239] and renting[$1,553] to remain the same or even increase. I belive in the housing bubble logic presented on Patrick.net. I want the spread to remain the same or increase because this means I get more value for my rental dollar and I get to stash money away for a down payment on a home. My stashed money gets invested in things like ETF and stocks. So we all know that housing cost are sky high and this article leads me to believe the median rent will increase beyond $1,553. According to The Housing Council of San Mateo County, 27 percent of households are living beyond their means (PDF) and renters need a salary of $61,440 to afford the average rent on a two bedroom aparment. We are all getting squeezed. Home owners living on the edge will fall off as ARMS ratchet upward and renters will be hard pressed to find a decent place for their families. Frankly it is too late for those who bought homes with the idea of flipping the home in a year or two. The slowing appreciation rate has singled the end of this game. However RENTERS now is your time to optimize your budgets, invest wisely and wait on the sidelines for the decline in Bay Area housing prices.

Friday, October 13, 2006

Market Madness

The Dow has pushed past previous "records" to hit new all time highs. Don't be fooled by these numbers. They do not reflect reality.

Never mind that the previous record was in January 2000 dollars. Inflation eaten up 15% (or more, unless you actually believe the government inflation numbers).

Never mind that the US dollar is worth 30% less in the world now than in 2000.

The fact of the matter is that the market index is reported in "nominal" dollars. It doesn't take into account the lower purchasing power of dollars today as compared to seven years ago.

If you had left your money in cash from 2000 to today, you would be up almost 21%.

Even accounting for dividends paid by Dow companies, this investment is barely break even for 7 years.

Since many ordinary investors buy the Dow through mutual funds, they are getting additional fees removed from their holdings, year after year after year. Over the 7 years, mutual fund fees of 1.5% would have removed another 10% from your nest egg.

Never mind that the previous record was in January 2000 dollars. Inflation eaten up 15% (or more, unless you actually believe the government inflation numbers).

Never mind that the US dollar is worth 30% less in the world now than in 2000.

The fact of the matter is that the market index is reported in "nominal" dollars. It doesn't take into account the lower purchasing power of dollars today as compared to seven years ago.

If you had left your money in cash from 2000 to today, you would be up almost 21%.

Even accounting for dividends paid by Dow companies, this investment is barely break even for 7 years.

Since many ordinary investors buy the Dow through mutual funds, they are getting additional fees removed from their holdings, year after year after year. Over the 7 years, mutual fund fees of 1.5% would have removed another 10% from your nest egg.

Thursday, October 12, 2006

You are responsible for your retirement, not your company

There was a time in American when it was not usually to work your entire life for one company and then retire with the security of knowing that every month a company retirement check would show up in your mailbox. As I am sure you realize those days are long gone. Outsourcing, mergers and overseas competition have changed the landscape of the America workforce. I work in IT and recent studies have shown that on average folks change companies every five years in IT.

Gone too are the days were a company would provide a pension plan to its employees. With a company pension plan every employee knew exactly how much money they would have when they retired. The companies funded the pension plan and the employee was not responsible for making any investment choices. The company took care of it all. When you retired you would get a retirement check for the REST OF YOUR LIFE.

Can you image the dismay felt by thousands United Airline workers when their company declared bankruptcy and was allowed by the courts to default on billions of dollars of employee retirement money? This is just one of several recent examples where company funded pensions have failed. The mantra of this posting is “you are responsible for your retirement”.

Most companies have shifted from company funded pension plans to 401(k) retirement plans. With these plans employees put a portion of their earning into tax-deferred investments. Sometimes a company will match a portion of the dollars the employee contributes. The two big differences between a traditional company funded pension plan and a 401(k) are:

- You are not guaranteed a retirement check for the rest of your life.

- The company provides a selection of investment choices and it is up to the employee to research and understand the investment choices.

You are responsible for your retirement, not the company. You, not the company, need to make sure you are not living in a run down apartment and eating canned food when you are 70 years old.

You need to save and invest for your retirement NOW. Time is your enemy. Now is the time to start taking responsible and learning about your 401(k) investment choices. Now is the time to start putting money aside each month to make investments. You need to make your money work for you now or you have no chance of enjoying the 20 or more years you expect to live when you retire.

As the first step I urge, beg and implore you to watch the PBS Frontline documentary entitled Can you afford to retire?. You can veiw the show for free online. The instructions state that you need Microsoft media player or Real Player. I cound not play the show using Media Play, but was able to using Real Player. If you do not have the time or bandwidth to watch the show online you can visit your local library and see if they have a copy.

The picture in this posting is meant to be distrubing I want you to seriously think about where you will be 10 years after you retire. Example: my rent is $1,000/month and my food bill is about $500/month. So food and housing is $1,500/month for me.

I want to live and have fun for at least ten years after I retire. How much do I need? $1,500 X 12 = $18,000 per year

10 years = $180,000

Now this is very basic and actually $180,000 won't even come close to being enough money to live on for ten years. The key is learn about investing and start making your money grow now. This is the only way to increase your chance of having the retirement you have dreamed of. Now go watch the video. Check back in at Pennyjar and let's learn together how to invest wisely.

Monday, October 09, 2006

Why Pay Commissions

Trade stocks for free.

Today, zecco.com debuted commission free stock trading.

$2,500 minimum balance

40 stock trades per month

Zecco makes money through advertising on the site, interest on cash balances and margin accounts and charges for some other things like options trading.

Zecco is a kind of stylized mesh of the words: Zero Commission Online

Today, zecco.com debuted commission free stock trading.

$2,500 minimum balance

40 stock trades per month

Zecco makes money through advertising on the site, interest on cash balances and margin accounts and charges for some other things like options trading.

Zecco is a kind of stylized mesh of the words: Zero Commission Online

Thursday, October 05, 2006

Direct stock purchase programs

Do you want to invest in the stock market but feel you do not have enough money to even join the game? It can be costly just to poney up the money to join a discount broker like Charles Schwab or Etrade. Charles Schwab requires a minium of $2,500 to open an account and Etrade requires $1,000. On top of that they charge you about $13.00 everytime you want to buy or sell a stock. Hardly a winning combination for a tight budget. However all is not loss (pun) there is a way for the little fish to get in on the action. For as little as $50 a month you can buy shares of blue chip companies. The secret is buying the stock directly from the company using a company's direct stock purchase program or DRIP (dividend reinvestment program). Not all companies provide these programs, but a signifcant number of well-known and well-run business do. A sample list of companies that sell stocks direct to the public are

O.K. now I have shown you a real life example of how you can join the big fish and own stocks for as little as $25/month. Believe it or not that is the easy part. My question to you is "So is (NYSE:BUD) a good stock to purchase? Is this stock right for your investment portfolio?" Yes that's right now that you can join the game you need to learn to play the game. Stay tune to PennyJar in the weeks to come I as we take a closer look at our bud-light friend and see if it is the kinda stock we think will make us some money

- McDonald (nyse: MCD)

- Walt Disney Co. (nyse: DIS)

- Intel (nasdaq: INTC)

- CVS (nyse: CVS)

O.K. now I have shown you a real life example of how you can join the big fish and own stocks for as little as $25/month. Believe it or not that is the easy part. My question to you is "So is (NYSE:BUD) a good stock to purchase? Is this stock right for your investment portfolio?" Yes that's right now that you can join the game you need to learn to play the game. Stay tune to PennyJar in the weeks to come I as we take a closer look at our bud-light friend and see if it is the kinda stock we think will make us some money

Stock Picking

At pennyjar we are always scouring the cyberworld for interesting and useful tools for the small stockpicker. Here are a couple of newer ones that have come up on our radar. Have fun.

Wednesday, October 04, 2006

Discretionary Income : choose your path

Let’s start of by defining discretionary income. It is a big word but a pretty basic concept. Discretionary income is defined as the amount of an individual's income available for spending after the essentials (such as food, clothing, and shelter) have been taken care of.

This basically means taking care of your needs before you worry about your wants. Now we have all been in situations where we have had to choose between what we need and what we want. For instance you need to pay your mortgage or rent but you want to take a vacation. You cannot have both and as grown ups we understand that we need to pay the rent and delay the vacation. Part of growing up is learning how to delay gratification and developing a sense of self-worth. How well we develop these two behaviors goes along way toward satisfying our basic needs and clarifying our wants from life.

The choices we make with our money are inexplicably tied to our behavior. Noted psychiatrist Dr. William Glasser developed “Rational Choice Theory”. Rational Choice theory postulates that people calculate the likely costs and benefits of any action before deciding what to do. The benefits of taking a vacation do not exceed the cost of losing a place to live. Like Maslow’s hierarchy of needs, Rational Choice theory believes humans are driven by the basic need for survival and the psychological needs of belonging, power, freedom and fun. So discretionary income is the money we have after we have taken care of our basic needs and is used to satisfy our psychological needs of belonging, power, freedom and fun. So once we have some "extra" money our goal should be learning how to effectively utilize discretionary income toward a better life. How does one effectively utilize discretionary income toward a better life? The first step is to understand the choices you have with discretionary income. To illustrate this I have created a road map named the Money Quadrant. Its purpose is to show the four basic paths you can choose with your deiscretionary income.

- Shopping

- Saving

- Gambling

- Investing

With wealth you will more often do things because you want to not because you have to.

Sunday, October 01, 2006

ETF vs.Traditional Mutual Funds